Advertisement

Advertisement

Dax Index News: Today’s Forecast Hinges on Middle East and Trade Headlines

By:

Key Points:

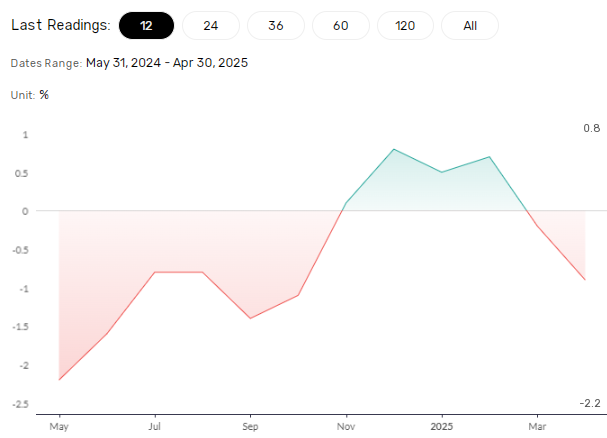

- German producer prices may sway ECB rate outlook—economists forecast a 1.2% YoY drop for May.

- DAX outlook hinges on Middle East conflict, US-EU trade tensions, and upcoming ECB and US economic data.

- DAX futures and Hang Seng rise on June 20 as easing fears of an imminent US strike boost sentiment.

DAX Slides to a Six-Week Low as US Attack Threats Spook Investors

Markets rattled as the DAX hit a six-week low on rising fears of US intervention in Iran. The DAX slid 1.12%, building on Wednesday’s 0.50% loss, closing at 23,057 on Thursday, June 19. Notably, the Index dropped to a six-week low of 23,052 before steadying.

Investor fears of US involvement in the Middle East conflict pressured risk assets as the Israel-Iran conflict raged on.

WTI crude oil hit a session high of $75.525 before closing the session up 1.21% at $73.585. US strikes on Iran could lead to a regional conflict, raising the threat of oil supply disruption. Rising oil prices may fuel inflationary pressures and affect economic momentum, delaying central bank rate cut plans.

On June 19, CN Wire reported:

“Iran’s military command Khatam Al-Anbiya warns US that any direct involvement will expand the conflict to the region and impose irreversible blows.”

Auto, Bank, and Tech Stocks Stumble

A potential escalation in the Middle East conflict triggered losses across auto, bank, and tech stocks.

Commerzbank and Deutsche Bank fell 1.63% and 1.31%, respectively. Oil supply disruptions could impact the global economy, affecting demand for credit and bank earnings.

Tech stocks SAP and Infineon Technologies ended the session down 2.06% and 0.44%, respectively.

Auto stocks also faced heavy selling pressure, with trade developments adding to the negative sentiment. BMW and Volkswagen slid 1.43% and 1.32%, respectively. Mercedes-Benz Group and Porsche also posted losses. According to CN Wire, European officials faced US resistance against lowering 10% US tariffs on EU goods, stating:

“European officials increasingly resigned to 10% baseline rate on reciprocal tariffs in any US-EU trade deal say sources familiar with talks.”

German Producer Prices to Spotlight the ECB

On Friday, June 20, Germany’s producer prices may influence the ECB rate path. Economists expect producer prices to fall 1.2% year-on-year in May after declining 0.9% in April. A sharper decline may fuel speculation about an ECB rate cut. Conversely, a higher print may support expectations of an ECB pause on rate cuts. Economists consider producer prices a leading inflation indicator.

US Futures Dip in Morning Trade

The US Futures markets posted losses ahead of the European opening bell on Friday, June 20. Rising oil prices, the Iran-Israel conflict, and Fed Chair Powell’s stance on tariffs and inflation remained headwinds. The Dow mini fell 106 points, while the Nasdaq 100 and S&P 500 dropped 38 and 12 points, respectively. US markets were closed on June 19.

Philly Fed Manufacturing Index in Focus

Later in the European session on June 20, the Philly Fed Manufacturing Index needs consideration. Economists expect the Index to rise from -4 in May to -1 in June. A higher print could ease US recession fears, boosting demand for risk assets, including the DAX. However, a sharp fall may revive speculation about a US recession, impacting sentiment.

While the data will influence risk appetite, trade developments, and Iran-Israel conflict-related news remain the key drivers.

Outlook: Key Catalysts for the DAX

The DAX’s near-term trajectory hinges on news from the Middle East, trade headlines, and ECB commentary.

- Bullish Case: Progress toward a US-EU trade deal, de-escalation in the Israel-Iran conflict, and dovish ECB signals could drive the DAX toward 23,500.

- Bearish Case: Threats of a US strike on Iran, rising trade tensions, or hawkish ECB rhetoric may drag the DAX toward 22,750.

At the time of writing on June 20, the DAX futures gained 162 points, tracking the Hang Seng Index higher. Easing fears of a US strike boosted demand for risk assets.

According to Polymarket, the chances of US military action against Iran by July stood at 60%, down from 90% on June 18.

Technical Setup Suggests Cautious Optimism

After Thursday’s sell-off, the DAX trades below the 50-day Exponential Moving Average (EMA), while remaining above the 200-day EMA. The EMAs send bearish short-term signals but longer-term bias remains bullish.

- Upside Target: A breakout above the 50-day EMA could support a move toward 23,500. A return to 23,500 may open the door to retesting 23,750.

- Downside risk: A break below 23,000 could expose 22,750.

The 14-day Relative Strength Index (RSI), at 37.56, indicates the DAX has room to drop below 23,000 before entering oversold territory (RSI< 30).

Conclusion: Middle East, Tariffs, and the ECB

Traders should closely monitor geopolitical developments, trade negotiations, and central bank commentary.

Explore our exclusive forecasts to assess whether improving trade sentiment could lift the DAX to new highs. Refer to our latest forecasts and macro insights here for further analysis, and consult our economic calendar.

About the Author

Bob MasonChief Crypto Boss

123456789 30 He has written extensively for a broader audience and his current focus is on developments relating to the financial markets including, but not limited to currencies, commodities, alternative asset classes, and global equities.

Advertisement